All Categories

Featured

Table of Contents

For lots of people, the greatest trouble with the unlimited financial idea is that first hit to early liquidity caused by the prices. Although this con of unlimited financial can be lessened significantly with appropriate policy design, the first years will constantly be the most awful years with any kind of Whole Life policy.

That claimed, there are certain boundless banking life insurance coverage plans developed mostly for high early money worth (HECV) of over 90% in the very first year. The long-lasting performance will usually significantly lag the best-performing Infinite Banking life insurance coverage policies. Having access to that extra 4 numbers in the very first couple of years may come with the price of 6-figures in the future.

You in fact obtain some substantial long-lasting benefits that aid you recover these very early expenses and after that some. We find that this prevented early liquidity issue with infinite financial is much more mental than anything else as soon as completely explored. As a matter of fact, if they absolutely needed every dime of the cash missing from their boundless financial life insurance policy policy in the first couple of years.

Tag: limitless financial concept In this episode, I speak concerning financial resources with Mary Jo Irmen who shows the Infinite Financial Principle. With the rise of TikTok as an information-sharing platform, monetary recommendations and techniques have discovered an unique means of spreading. One such strategy that has actually been making the rounds is the unlimited financial idea, or IBC for short, gathering recommendations from stars like rapper Waka Flocka Fire.

Within these policies, the cash value grows based upon a price established by the insurance firm. Once a substantial cash value collects, insurance policy holders can acquire a money value lending. These fundings vary from traditional ones, with life insurance policy acting as collateral, indicating one might lose their protection if borrowing exceedingly without adequate money value to support the insurance coverage expenses.

And while the allure of these policies appears, there are innate limitations and threats, requiring attentive cash worth surveillance. The strategy's legitimacy isn't black and white. For high-net-worth individuals or local business owner, particularly those making use of methods like company-owned life insurance policy (COLI), the benefits of tax obligation breaks and compound growth might be appealing.

Whole Life Insurance For Infinite Banking

The appeal of boundless banking doesn't negate its difficulties: Cost: The fundamental need, a long-term life insurance policy, is pricier than its term equivalents. Qualification: Not everyone gets approved for whole life insurance policy because of rigorous underwriting processes that can omit those with specific health or lifestyle problems. Intricacy and danger: The detailed nature of IBC, coupled with its threats, might discourage lots of, particularly when less complex and less risky options are readily available.

Designating around 10% of your regular monthly revenue to the plan is simply not viable for the majority of people. Utilizing life insurance policy as a financial investment and liquidity source needs self-control and monitoring of policy cash money value. Seek advice from a financial expert to figure out if unlimited banking aligns with your concerns. Component of what you read below is simply a reiteration of what has already been claimed above.

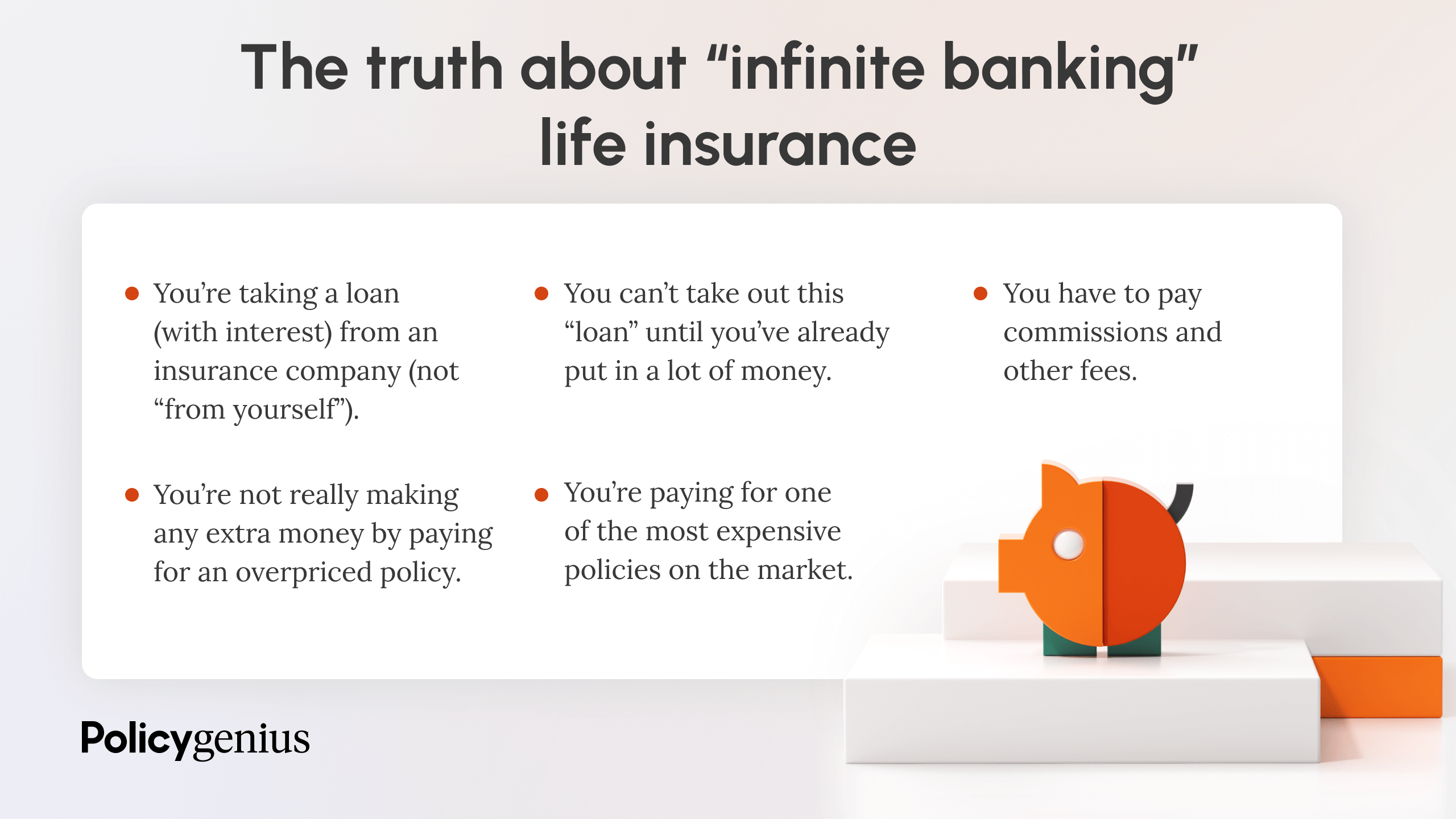

So before you get on your own into a scenario you're not gotten ready for, recognize the complying with first: Although the principle is generally offered because of this, you're not actually taking a finance from yourself. If that were the case, you wouldn't have to repay it. Instead, you're borrowing from the insurance provider and have to settle it with passion.

Some social media posts suggest using cash money value from entire life insurance coverage to pay down credit scores card financial obligation. When you pay back the financing, a part of that interest goes to the insurance policy business.

For the very first several years, you'll be settling the payment. This makes it very tough for your plan to accumulate worth during this time. Whole life insurance coverage expenses 5 to 15 times a lot more than term insurance policy. Most individuals simply can not manage it. So, unless you can manage to pay a couple of to several hundred bucks for the next decade or even more, IBC will not benefit you.

Be Your Own Banker Life Insurance

If you need life insurance policy, right here are some beneficial tips to take into consideration: Think about term life insurance coverage. Make certain to go shopping about for the finest price.

Copyright (c) 2023, Intercom, Inc. () with Booked Font Style Call "Montserrat". This Font style Software program is certified under the SIL Open Up Typeface License, Variation 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Scheduled Font Call "Montserrat". This Font Software application is licensed under the SIL Open Up Font Certificate, Version 1.1.Miss to major content

Ibc Concept

As a CPA specializing in property investing, I've combed shoulders with the "Infinite Financial Idea" (IBC) much more times than I can count. I have actually also interviewed specialists on the topic. The major draw, other than the noticeable life insurance coverage benefits, was always the concept of developing money value within a long-term life insurance policy plan and borrowing versus it.

Certain, that makes good sense. However truthfully, I constantly thought that cash would certainly be much better invested directly on investments instead of funneling it through a life insurance policy plan Until I discovered how IBC can be combined with an Irrevocable Life Insurance Policy Trust (ILIT) to produce generational wide range. Let's start with the fundamentals.

Bank On Yourself Complaints

When you obtain versus your policy's money worth, there's no set payment schedule, providing you the freedom to take care of the finance on your terms. Meanwhile, the cash money value continues to expand based upon the plan's warranties and dividends. This configuration allows you to accessibility liquidity without interfering with the long-lasting growth of your plan, offered that the funding and passion are taken care of sensibly.

The procedure continues with future generations. As grandchildren are birthed and expand up, the ILIT can purchase life insurance policy policies on their lives. The count on after that collects multiple plans, each with expanding money worths and death benefits. With these policies in position, the ILIT properly comes to be a "Family Financial institution." Relative can take fundings from the ILIT, making use of the money value of the policies to fund financial investments, start services, or cover significant expenditures.

A crucial facet of handling this Family Bank is making use of the HEMS criterion, which means "Wellness, Education And Learning, Upkeep, or Support." This guideline is usually included in depend on arrangements to direct the trustee on how they can distribute funds to recipients. By adhering to the HEMS criterion, the depend on ensures that distributions are produced necessary needs and long-lasting assistance, securing the count on's possessions while still offering family participants.

Increased Adaptability: Unlike rigid small business loan, you manage the settlement terms when borrowing from your very own policy. This permits you to structure repayments in a manner that lines up with your company money circulation. nelson nash infinite banking book. Improved Capital: By funding overhead via policy fundings, you can possibly maximize cash money that would otherwise be locked up in typical car loan repayments or equipment leases

He has the exact same devices, however has also built additional cash value in his plan and received tax obligation advantages. And also, he currently has $50,000 available in his plan to utilize for future opportunities or costs. Despite its potential benefits, some people continue to be cynical of the Infinite Banking Idea. Let's address a few usual problems: "Isn't this just costly life insurance policy?" While it's real that the premiums for a properly structured entire life plan might be greater than term insurance coverage, it is very important to view it as even more than just life insurance policy.

How Infinite Banking Works

It's regarding developing a flexible funding system that provides you control and supplies several advantages. When utilized tactically, it can match other financial investments and business techniques. If you're fascinated by the capacity of the Infinite Banking Principle for your organization, here are some steps to take into consideration: Educate Yourself: Dive much deeper right into the concept via trusted books, seminars, or examinations with knowledgeable specialists.

{kind=link}

Latest Posts

How To Start Your Own Personal Bank

Cibc Aerogold Visa Infinite Online Banking

Infinite Credit Loan